Dollar cost averaging is one of the most popular and basic investing tips out there when it comes to basic theory and practice. There are many positives, and a few negatives worth considering if you’re going to dollar cost average your investments rather than use a different method. To put the real results into perspective though, I crunched some numbers of how you would have fared over the past 10 years if you had performed any of three different investment methods:

- Dollar Cost Average Monthly – I modeled $1000 invested at the closing market price every month for 10 years. Total investment was $120,000.

- Dollar Cost Average Annually – I modeled $1200 invested at the closing market price every year for 10 years. Total investment was $120,000.

- Initial One-Time Investment – I modeled a single one-time investment of $120,000 at the start of the 10 year period.

Assumptions:

- I used the Nasdaq as my proxy – QQQ ETF (for more on ETF investing in indices, leveraged ETFs, commodities and more, visit my other site ETFBase.com). The reason I used QQQ instead of the more common SPY representing the S&P500 was two-fold. First off, the Nasdaq is more volatile and whatever thesis results from this exercise would be more pronounced. And after all, if you’re investing for the long-term and anticipate stock prices always move up over long enough periods of time, you want to be in higher beta investments. Secondly, I also wanted to minimize the impact of dividends. See, I was kinda lazy and was looking for a directional/magnitude result here and didn’t want to complicate things by having to include dividend payments each quarter, reinvesting those dividends, etc. Since the dividend yield on QQQ is less than half that of SPY, the effect of ignoring dividends is much more palatable for this exercise.

Results

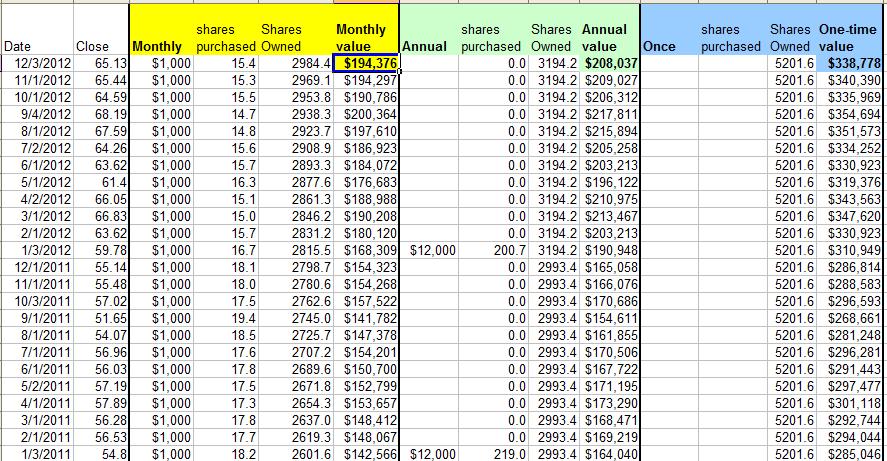

I’m including a screen shot of the raw data and a graphical representation of the results. What you’ll find is that of course, because the index was up relatively substantially over a 10 year period, you’d have been better off having invested all your money up-front rather than dollar cost averaging along the way. Now, you may just think, “anyone confronted with the options would always do that since the returns would be higher”. But no, to the contrary, the human psyche plays games of guilt on us. Many people are so risk averse that even if they had $120,000 laying around today, they would NOT invest it as a lump sum. They would sooner hold some in cash and gradually invest it into an index over many years in a dollar cost average fashion rather than invest it all at once. They figure (rightly so) that if they invest at a lousy interval like right before a major crash, they won’t lose 50% of their investment within a short period of time. So, there’s no right answer here looking forward. Historically, most times you’d have been better off having invested up front but of course if you cherry pick a start date just prior to a crash, the results will be to the contrary.

(click to enlarge)

Regardless, for the most recent 10 year period, here are the actual results:

- Dollar Cost Average Monthly – $194K

- Dollar Cost Average Annually – $208K

- Initial One-Time Investment – $339K

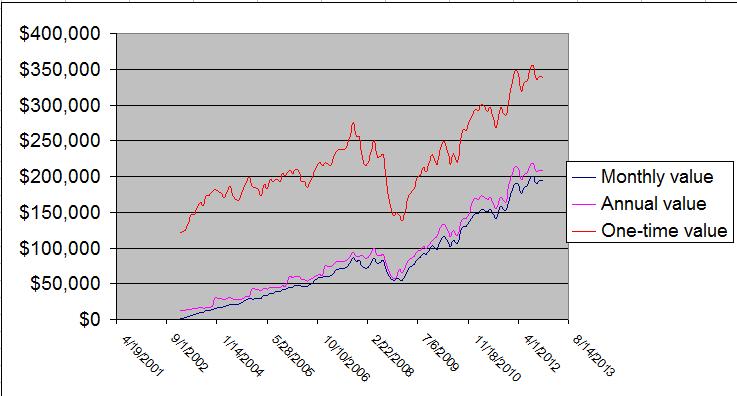

(click to enlarge)

It’s interesting to note that there’s not much difference at all whether you invested monthly or annually, but the one-time investment showed a huge gain, almost tripling your money over the 10 year period. This would probably be a triple if you threw in the dividends, which I excluded of course.

If dollar cost averaging is something you’re interested in, there are some great low-cost online investment houses, some of which are offering signup bonuses right now. Use one of these links to get the following promotions:

- Â OptionsHouse – 100 Free Trades with a New Account

- ETrade – Trade free for 60 days and get up to $500 in Bonuses

- OptionsExpress – $100 Bonus with a new account

If you’re going to start dollar cost averaging or trade in general, you might as well get a bonus even if you have a few accounts! (I do).

And of course, to keep track of it all in a nifty, no-hassle format so you can see your net worth every day, just sign up for a free account with Personal Capital.

Do You Dollar Cost Average?

{ 22 comments… read them below or add one }

Vanguard did a research on this and came to the same conclusion. Since the market has the tendency to go up in the long term, it’s better to have more of your money in play. I’m surprise that there is so little difference between monthly and annually though.

I rolled over my 401k last year and I got paralyzed for a few days. Luckily I got over it and invested all of it before the latest run up.

My thinking exactly

I agree this works in a good market, but what happens if you do the same exercise for a five year period 1/1/2008 – 12/31/2012? I would assume they would be much closer.

I’ll have to take a look! (file on other computer…grrrrr…)

I generally haven’t had the large sum up front to invest so I’ve gone for DCA, though this past year I didn’t invest at all since I had taken the leap of faith. 😉 I gotta see for this year.

good luck!

The main problem with dollar cost averaging is that you will essentially pay more than the investment is worth over time. If you simply invest a lump sum when a stock is trading at a significant discount to intrinsic value you are much more likely to succeed and make big returns over the long term.

Yeah, it only works out better if you invest into a flat or falling market, which, if that’s what you anticipate then why invest in that asset class at all?!

The only problem with this argument is that it’s not too often we receive a large windfall. We generally earn our money incrementally, so while investing $120k today may be better than spreading that investment across 10 years, I don’t have $120k in cash sitting around to invest today. The more likely scenario is that by the time I’ve earned $120k, I’ve already been incrementally investing each month as my paycheck comes in. And surely it’s better to incrementally invest as the money comes in rather than stockpiling it until you have a large lump sum to invest just because data shows that lump sum investments are better than dollar cost averaging.

That’s why I don’t really like calling it “dollar cost averaging.” That’s not what I’m doing. I’m not investing a little bit each month because I believe it’s a good strategy to mitigate risk, I’m doing it because that’s how the money comes in: a little bit each month. Unless you just received a windfall and have a large amount of cash sitting in your bank account, investing little bits each month isn’t dollar cost averaging, it’s just incrementally investing as money becomes available to invest.

There is nothing wrong with storing that monthly input into a cash account until you’re ready to invest a lump sum.

If I had the money coming in monthly, I’d probably invest as-is, but lump sum situations do certainly arise for regular people.

Sure, there’s nothing wrong with it, but you’re missing out on gains while it’s sitting in a savings account. The logic is actually the same as the logic in the article – you want your money to be invested for as long as possible. The difference is just the starting point. If you start with a large sum, it’s likely better to invest it all at once rather than dollar cost average. But if you start with nothing and you receive small amounts of money on a regular basis, you still want to get that money invested earlier rather than later, so you’d be better off “dollar cost averaging” than sitting on the cash until you have a big lump sum to invest.

I wouldn’t call windfalls “common” but they’re not uncommon either. Here are a few situations that have happened to various friends and family just within our circle – inheritance, settlement from a car accident, settlement from employer lawsuit, settlement from divorce, retirement w lump sum pension payment. Those are just a few off the top of my head. These situations do arise here and there, so definitely worth thinking about!

Very interesting! Doesn’t it still matter when you invest the lump sum?

Sure, like I mentioned, if you pick the pivot top and the market crashes, then you feel terrible and the results will differ. That’s the risk you take! What are the odds you pick the worst possible time to invest? Probably low, but that’s what deters people from doing it!

Great post! I remember seeing a similar analysis in Siegal’s book, Stocks for the Long Run, that came to the conclusion that it is better to lump sum invest than spread it out.

Oh I figured there are tons of people that did this work before me; was fun to crunch the numbers; glad at least some respectable authors agree!

This is not dollar cost averaging. A good dollar cost averaging example would have shown the difference between investing daily or weekly over the course of a year vs. investing it all at the beginning of the year, with the results for various performance scenarios. DCA just minimizes risk by averaging your cost over the course of a year, rather than investing it all at the price listed on day 1.

All you’re showing is the effect of compounding over 10 years in the above example. That’s not a bad thing to demonstrate, but don’t call it dollar cost averaging!

Seriously? You’re not making sense. How is the example NOT dollar cost averaging? It is. Just because you don’t like the data doesn’t mean you change the definition. Vast majority of Americans are paid weekly, bi-weekly or monthly and hence, investments go in on that schedule. Not daily.

I am only just beginning to learn the ins and outs of investing. I have always wondered which of the two would earn more (lump sum or spread out). I am glad to see that other people have actually made the computation. A brokerage firm here in the Philippines, have adopted the same strategy aptly called Peso Cost Averaging. They encourage people to regularly invest over longer periods of time (10 to 20 years) in one or a select few trusted companies only. But the general consensus I’ve been reading is to not invest it all at once. Maybe there are other differences between DCA and PCA that I do not konw yet. I guess I have more reading to do.

Great analysis, and this is what I did for 25 years. It worked out OK, but thankfully I wasn’t bound to the decision. Your point about hitting an inflection is well-taken; with the NASDAQ close to 5,000 in 2000, a lump-sum deposit to QQQs ETF would still be heartbreaking to look at 13 years later. Same with the NIKKEI, 20 years later investors are crying in their sake.

At this point, I cannot feel comfortable about investing in a stock market dependant upon Fed intervention and artificially low interest rates. I have been easing money out of the stock market, and into cash instruments; I have missed a good part of some upside, but having caught that downside of -50% in 2003 and -57% in 2007-09, I am quite comfortable in eliminating the risk of suffering that kind of downside, going forward. But that is only because my “long-term” is 25 years shorter than your younger readers, and my ability to make up losses in time and money is no longer available. If I was 30, I would do exactly what your analysis showed and put the money in the market as soon as I could.

I’ve seen this argument about dollar-cost versus lump sum investing before. What if always fails to include, however, is rebalancing in a diversified portfolio. An annual rebalancing of (e.g.,) a 40% bonds, 60% index equities (subdivided into domestic and international markets) mix would make for a much more complicated discussion. In years where bonds were low, you’d be buying them at a discount and switching some equity money there, and vice-versa. Any idea on how rebalancing would change these performances? …Is it irrelevant maybe?

I’m not a math whizz kid, but I assume that dollar-cost-averaging must be used in conjunction with rebalancing in order to work correctly. …Yeah or am I delusional?