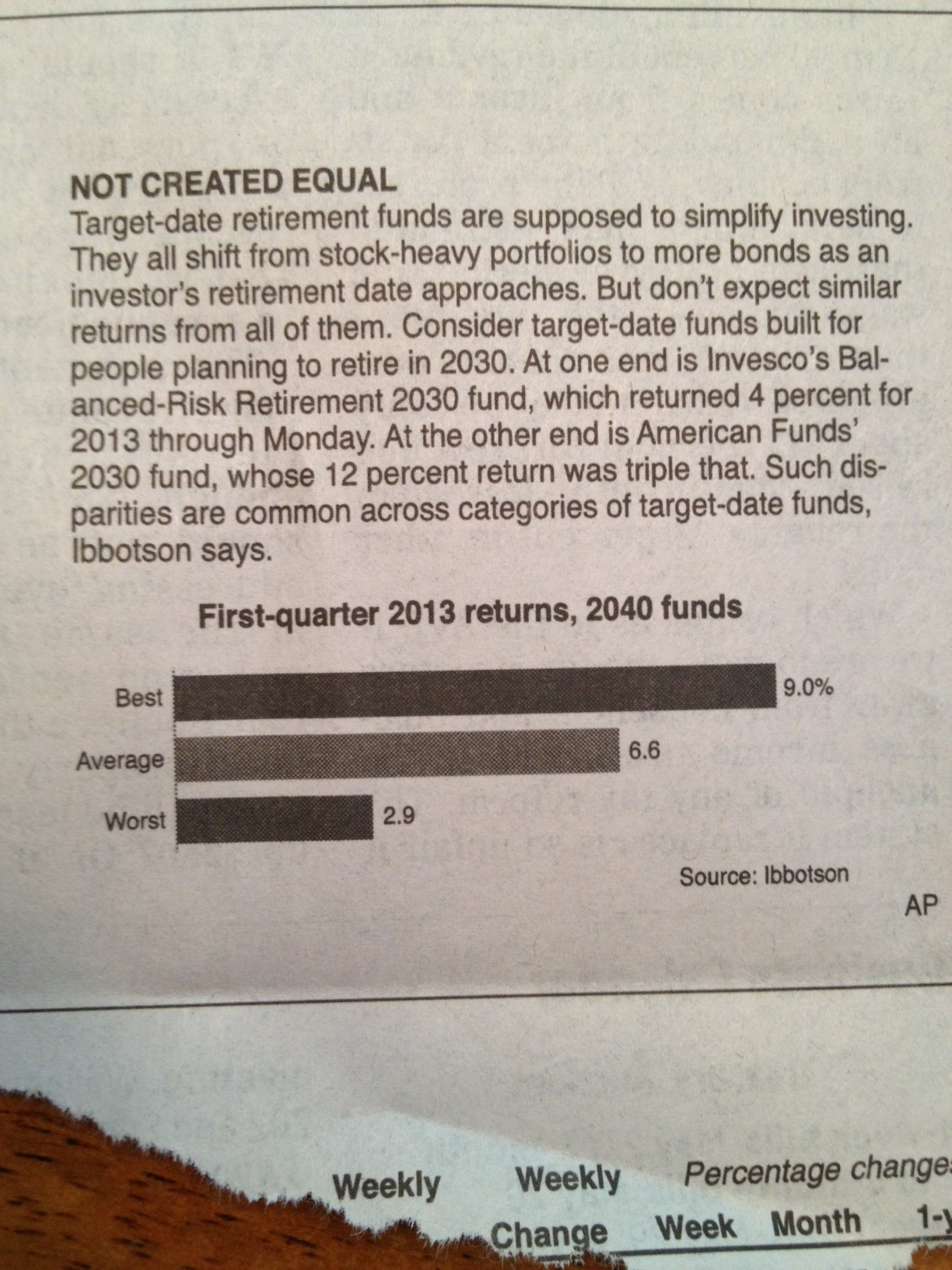

I was reading my local paper today and it reminded me of the shenanigans that continues to ensue with respect to “Target Date Funds”. Many investment plans and almost all major mutual fund companies now offer these target date funds that claim to provide the right mix of stocks and bonds (basically, to optimize returns vs. volatility) for investors based on their age. Aside from the fact that everyone’s risk tolerance and actual investment objectives are different, the funds themselves have wildly divergent returns for the same target year. For instance, take a look at this snapshot of various 2040 funds. How can one have a 1Q2013 return of 9.0% while another has a return of 2.9%? That’s insane. I’d be annoyed if I were a 20-something or 30-something that thought I was getting a relatively high performing mix of primarily stocks and yet the fund only returned 2.9%, especially when paying a higher fee (see how bad the fees are on target date funds). Here’s the snapshot:

An additional consideration is that it’s a bit of a misnomer to classify any of the funds as “best” and “worst” as the article portrays. All these returns really indicate is that one fund had a higher mix of stocks than the other. So, in a downturn, that “best” fund would vastly underperform and lose more money as well and end up in the “worst” category instantly.

How to shield yourself from all this nonsense and actually achieve better returns? Buy the lowest cost index funds you can get your hands on instead and balance yourself as you age. These target date funds tend to have much higher expense ratios and don’t accomplish anything you can’t do yourself. Over a decades-long period of time, enjoying lower annual expenses will boost your retirement fund returns much more than trying to pick the right actively manager and target date funds. These are the facts.

Do You Use Target Date Funds?

{ 8 comments… read them below or add one }

It’s probably pretty easy to find what those funds are actually using… I wonder if any of them are using some bad active managers that further lower their returns. As you noted a few years of low returns doesn’t mean much but some of these funds might be set up to deliver permanently low returns.

I never liked target date funds! I would rather take control of my investing. That way I am rewarded or penalized for my actions. Besides, using index funds keep it rather simple.

I’m not a huge fan of target date funds. Wrote about this once, and basically noted that it’s the control aspect that I want to have, and this includes the ability to rebalance when I want to – not when dictated by someone else.

Good post. The flip side of this is a chart that JP Morgan funds puts out on its advisor website that shows the allocation to stocks of 40+ TDF families for the fund designed for someone closest to retirement (at this juncture the 2015 fund in most cases). The range is from about 25% to 70% last time I checked.

I like TDFs for younger retirement plan participants (like my 2010 grad daughter in her 1st job). The longer-dated funds (Vanguard in her case) are aggressive and provide an instantly diversified portfolio. However I’m not a fan for someone within say 15-20 years of retirement. These folks need a portfolio tailored to their financial plan.

Target funds are the new money makers for investment firms. According to new rules if an employee doesn’t pick funds to invest in in his/her 401K, a target fund is chosen. You’ll be amazed how many do this – too lazy or ignorant to pick decent funds. So yes these make a lot of money!

Well spotted Darwin!

Auto-enrollment has its benefits…except when they put you in a lousy fund! Probably a liability thing, as they view it as less prone to crash than a straight equity index fund.

Another problem with them is that they charge a fee on top of the fee charged by the funds they are investing in!

That’s a great point. Hidden fees piled atop already high disclosed fees. Really eats into returns!

{ 1 trackback }